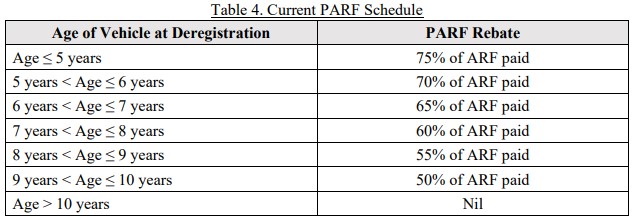

The International Accounting Standards Board (IASB) has issued IFRS 18 – Presentation and Disclosure in Financial Statements, which introduces a comprehensive restructuring of the statement of profit or loss and significantly expands disclosure requirements. Singapore is expected to adopt IFRS 18 into SFRS(I) for annual periods beginning on or after 1 January 2027, with full retrospective application.

Mandatory New Presentation Structure

Standardised Profit or Loss Categories

IFRS 18 introduces three mandatory, principle-based categories into the statement of profit or loss:

Operating

Investing

Financing

All income and expense items must be classified within these categories based on detailed application guidance. This represents a fundamental shift from existing practice, which allows more judgement in defining intermediate performance measures. The new structure aims to enhance cross-entity comparability and reduce diversity in practice.

Prescribed Subtotals

The standard introduces consistent subtotals across entities, such as:

Operating profit

Profit before financing and income taxes

Entities may no longer present bespoke subtotals unless they qualify as a Management-Defined Performance Measure (MPM) under the new disclosure framework.

Management-Defined Performance Measures (MPMs)

IFRS 18 establishes a specific framework for Management-Defined Performance Measures, defined as subtotals of income and expenses that:

Are used in public communications outside the financial statements; and

Reflect management’s view of an aspect of the entity’s overall financial performance.

Examples include Adjusted EBITDA, “core profit,” or other non-IFRS performance metrics commonly used in investor reporting.

For each MPM, entities must:

Provide a clear definition and description

Present a quantitative reconciliation to the nearest IFRS-defined subtotal

Disclose explanations of adjustments, including their nature and rationale

Present comparative information consistently across periods

This introduces discipline, transparency and comparability around non-GAAP performance metrics historically communicated without standardised requirements.

Enhanced Disaggregation Requirements

IFRS 18 tightens the requirements for disaggregation of income and expenses, requiring entities to:

Provide more granular breakdowns where necessary for users to understand performance

Avoid broad, aggregated line items such as “other expenses” unless immaterial

Apply a consistent basis for classification across the financial statements and notes

The standard specifies factors to assess whether items require further disaggregation, including nature, function, measurement basis, and variability.

Disclosures of “Unusual” Income and Expenses

IFRS 18 introduces explicit requirements to disclose unusual income and expense items, defined as items that:

Are not expected to recur in the near term; and

Have a significant effect on financial performance.

Entities must:

Identify such items based on the standard’s criteria

Disclose the amount, nature, and reason the item is considered unusual

Present comparative disclosures

This enhances users’ understanding of non-recurring items affecting performance trends.

Retrospective Application and Comparative Information

The standard requires full retrospective application, including:

Restating all comparative periods using the new P&L structure

Reclassifying historical income and expense items into operating, investing, and financing categories

Applying MPM definitions and reconciliations consistently to prior periods

Providing comparative disclosure of unusual items and disaggregation detail

As a result, entities presenting FY2027 financial statements will also present restated FY2026 comparatives under the IFRS 18 framework.

Implications for Reporting, Systems and Communications

The structural changes introduced by IFRS 18 will have significant implications for:

Financial statement presentation and mapping

Internal reporting frameworks

KPI and performance metric definitions

Investor and lender communication

Disclosure controls and accounting policy frameworks

Given the mandatory retrospective application and shift to standardised categories and subtotals, the adoption of IFRS 18 represents one of the most material presentation changes since the adoption of IFRS itself.

If you require technical guidance on IFRS 18 interpretation, presentation impacts, or disclosure implications, our team can support you with detailed analysis and implementation expertise.